WHAT HAPPENS WHEN I AM LAID OFF? Understanding the redundancy payment options is an important starting point

TWO TYPES OF REDUNDANCY PAYMENT OPTIONS

Redundancy payment options can seem highly complex to those that are enduring a significant life event. This is why it is important to take the time to carefully consider them and any long-term impact on future benefits

Frank Conway – Founder of MoneyWhizz

What is Statutory Redundancy Payment?

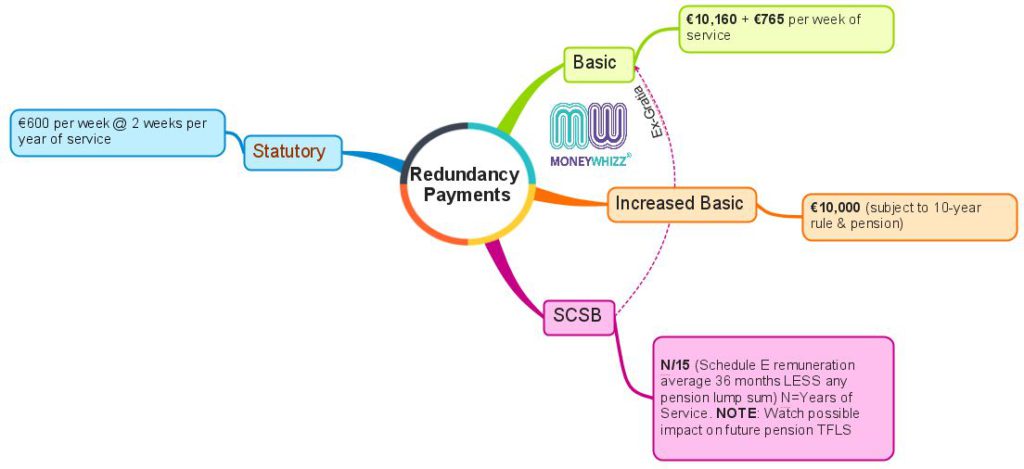

This is a lump sum payment which is based on your pay. Eligible staff members receive two weeks’ pay for every year of service along with an additional week’s pay. This payment has a maximum earnings limit of €600 per week. Using the example from the MyWelfare calculator, here is the breakout of how a payment is calculated.

What are Ex-Gratia Redundancy Payments?

Legally, your employer only needs to pay you the statutory redundancy payment if you are made redundant. However, some employers also offer an ex-gratia payment which is another way of saying payments above the legal minimum.

WHICH EMPLOYEES ARE COVERED?

You are eligible for a statutory redundancy payments if you meet the following criteria:

- Aged 16+

- Be in employment insurable according to the Social Welfare Acts. If you are aged 65 or less, you must also be paying Class A PRSI.

- You need to have worked continuously for the same employer for a minimum of two years over the age of 16.

- You must be made redundant.

The statutory redundancy payment is tax-free.

Taxation of lump sums

If you receive a redundancy payment lump sum in compensation for the loss of employment, part of it may be tax-free. The statutory redundancy lump sum is always tax-free. You can access the Citizens Information website to read more about taxation of lump-sum payments on redundancy/retirement. Additionally, there is more information about taxation and redundancy on the Revenue website.

On a redundancy or retirement payment, you are entitled to one of the following tax exemption options, whichever is the higher.

Basic Exemption and Increased Exemption

The Basic Exemption redundancy payment is €10,160, plus €765 for each complete year of service. (This does not include statutory redundancy which is tax free.)

An Increased Exemption of an additional €10,000 on top of the Basic Exemption is available in certain circumstances. You can get the Increased Exemption if you haven’t received a tax-free lump sum in the last 10 years and you are not getting a lump sum pension payment now or in the future.

If you are in an occupational pension scheme, the Increased Exemption is reduced by any tax-free lump sum from the pension scheme you may be entitled to receive.

Standard Capital Superannuation Benefit (SCSB)

This SCSB is a tax relief that normally benefits people with higher earnings and long service. It can be used if the following formula gives an amount greater than either basic exemption or Basic Exemption plus Increased Exemption.

Formula for SCSB: Take the average annual earnings over the previous 3 years (or the whole period of service, if less than 3 years), multiply this figure by the number of years’ service; divide by 15 and subtract the lump sum superannuation payment received or that may be receivable.

Example: You were made redundant in 2014 after 20 years’ service and received a lump sum of €100,000 which is your first lump sum. You also got a lump sum of €20,000 from your pension scheme. Your pay for the last 3 years before the date of leaving work was €180,000. The amount of the lump sum which is exempt from tax is the higher of the following 2 calculations:

- The Basic Exemption is:

€10,160 + €15,300 ( €765 x 20 years) = €25,460

There is no Increased Exemption as the pension scheme lump sum of €20,000 is greater than €10,000 - The Standard Capital Superannuation Benefit (SCSB) is:

€180,000 ÷ 3 x 20 ÷ 15 – €20,000 = €60,000

The taxable amount of your lump sum is €40,000 (€100,000 – €60,000). As the above example shows the SCSB tax relief of €60,000 is a higher amount of tax relief than the Basic and Increased Exemptions of €25,460.

Calculation of tax on redundancy payments

A certain amount of your redundancy payment is tax free, as described above, and the balance will be taxed. This is taxed as part of the current year’s income.

Previously there was a second method based on your average rate of tax for the previous 3 years. This was known as Top Slicing Relief which was not available on lump sums of €200,000 or more paid on or after 1 January 2013 and was abolished for all ex-gratia lump sum payments made on or after 1 January 2014.

The amount of your lump sum that is subject to tax is not subject to social insurance (PRSI), but the Universal Social Charge may be payable (Source: Citizens Information).

Once any redundancy payments options process is completed, it is important for those impacted to put in place a robust budgeting process at home.

Comments are closed.