The business start up process requires a lot of moving parts are considered and put in place to ensure the best chance for future success. In this article, we examine what are the primary considerations and how to tackle them.

Table of Contents

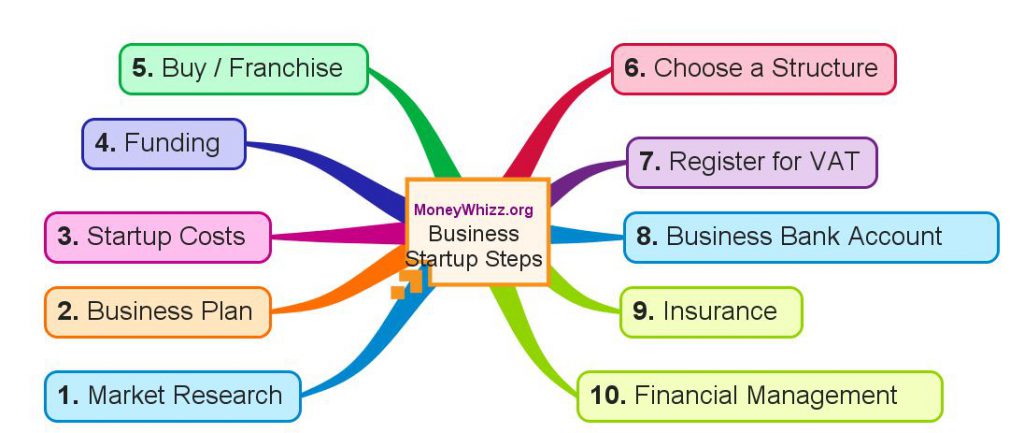

1. Market research and competitive analysis

As you set about your business startup process, it is important to keep in mind that good market research helps you find customers for your business. Competitive analysis helps you make your business unique. Combine them to find a competitive advantage for your business.

Market research blends consumer behaviour and economic trends to confirm and improve your business idea. It’s crucial to understand your consumer base from the outset. Market research lets you reduce risks.

It is important to gather as much demographic information as you can to better understand opportunities and limitations for attracting customers. This could include population data on age, wealth, family, interests, or anything else that’s relevant for your business.

Next, see if you can answer these questions to get a good sense of your market.

- Demand: Is there a desire for your product or service?

- Market size: How many people would be interested in your offering?

- Economic indicators: What is the income range and employment rate?

- Location: Where do your customers live and where can your business reach?

- Market saturation: How many similar options are already available to consumers?

- Pricing: What do potential customers pay for these alternatives?

Here are a few methods you can use to do direct research:

- Surveys

- Questionnaires

- Focus groups

- In-depth interviews

Your competitive analysis should identify your competition by product line or service and market segment. Assess the following characteristics of the competitive landscape:

- Market share

- Strengths and weaknesses

- Your window of opportunity to enter the market

- The importance of your target market to your competitors

- Any barriers that may hinder you as you enter the market

- Indirect or secondary competitors who may impact your success

2. Write your business start up plan

Your business plan is the foundation of your business. Learn how to write a business plan quickly and efficiently with a business plan template. Business plans help you run your business. A good business plan guides you through each stage of starting and managing your business. You’ll use your business plan as a roadmap for how to structure, run, and grow your new business. It’s a way to think through the key elements of your business.

Business plans can also help you get funding or bring on new business partners. Investors want to feel confident they’ll see a return on their investment. Your business plan is the tool you’ll use to convince people that working with you — or investing in your company — is a smart choice.

A quick online search will offer a range of different options for the development of a business plan. Pick a business plan format that works for you. There’s no right or wrong way to write a business plan. What’s important is that your plan meets your needs.

Most business plans fall into one of two common categories:

- Traditional or

- Lean startup.

Traditional business start up plans are more common, use a standard structure, and encourage you to go into detail in each section. They tend to require more work upfront and can be dozens of pages long.

Lean startup business plans are less common but still use a standard structure. They focus on summarising only the most important points of the key elements of your plan. They can take as little as one hour to make and are often only one page long.

3. Calculate your startup costs

How much money will it take to start your small business? Calculate the startup costs for your small business so you can request funding, attract investors, and estimate when you’ll turn a profit. Having a clear understanding your expenses will go a long way to helping you launch successfully.

Calculating startup costs helps you:

- Estimate profits

- Do a breakeven analysis

- Secure loans

- Attract investors

- Save money with tax deductions

- Identify your startup expenses

Most businesses fall into one of three categories:

- Brick-and-mortar businesses,

- Online businesses, and

- Service providers.

You’ll face different startup expenses depending on your business category.

There are common startup costs you’re likely to have no matter what. Look through this list, and make sure to add any other expenses that are unique to your business.

- Office space

- Equipment and supplies

- Communications

- Utilities

- Licenses and permits (Builders, electricians, physiotherapist…)

- Insurance

- Accountant and solicitor

- Inventory

- Employee salaries

- Advertising and marketing

- Market research

- Printed marketing materials (Graphic design)

- Building a website

Estimate how much your expenses will cost – once you have your list of expenses, you can estimate how much they’ll actually cost. This process will be different for each expense you have.

Some expenses will have well-defined costs — certifications and licensing requirements generally have clear, published costs. You might have to estimate other costs that are less certain, like employee salaries etc. Look online and talk directly to mentors, vendors, and service providers to see what similar companies pay for expenses.

Add up your expenses for a full financial picture – once you’ve identified your business expenses and how much they’ll cost, you should organise your expenses into one-time expenses and monthly expenses.

One-time expenses are the initial costs needed to start the business. Buying major equipment, hiring a graphic designer to design a logo (you can do this online yourself if you have a little creative flair but remember, a great logo can work wonders for a company so regard it as a very important investment). Make sure to keep track of your expenses and talk to your accountant when it’s time to file your taxes.

Monthly expenses typically include things like salaries, rent, and utility bills. You’ll want to count at least one year of monthly expenses, but counting three to five years is ideal.

Add up your one-time and monthly expenses to get a good picture of how much capital you’ll need and when you’ll need it.

4. Fund your business

It costs money to start a business. Funding your business is one of the first and most important financial choices most business owners make. How you choose to fund your business could affect how you structure and run your business.

Determine how much funding you’ll need – every business has different needs, and no financial solution is one size fits all. Your personal financial situation and vision for your business will shape the financial future of your business.

Once you know how much start-up funding you’ll need, it’s time to figure out how you’ll get it. These are some of the most common funding routes for business startups:

Self-funding – from your own resources, including savings or family support

Loans – you will need to demonstrate you have done your research and offer evidence of how you plan to repay.

Investors – generally will seek a stake in the business.

5. Buy an existing business or franchise

Starting a business from scratch can be challenging. Franchising or buying an existing business can simplify the initial planning process. Know the difference between franchising and buying a business.

Before you decide if one of these options is right for you, make sure you know the basics of franchising and buying an existing business. The main difference between franchising and buying an existing business is the level of control you’ll have over your business.

Franchising gives you more guidance but less control – a franchise is a business model where one business owner (the “franchisor”) sells the rights to their business logo, name, and business model to an independent entrepreneur (the “franchisee”). Restaurants, hotels, and service-oriented businesses are commonly franchised.

Two common forms of franchising are:

- Product/trade name franchising: The franchisor owns the right to the name or trademark of a business, and sells the right to use that name and trademark to a franchisee. This style of franchising normally focuses on supply chain management. Typically, products are manufactured or supplied by the franchisor and delivered to the franchisee to sell.

- Business format franchising: The franchisor and franchisee have an ongoing relationship. This style of franchising normally focuses on full-spectrum business management. Typically, the franchisor offers services like site selection, training, product supply, marketing plans, and even help getting funding.

When you buy a franchise, you get the right to use the name, logo, and products of a larger brand. You’ll also get to benefit from brand recognition, promotions, and marketing. It also means you have to follow rules from the larger brand about how you run your business.

Buying an existing business gives you more control but less guidance

Buying an existing business is exactly what it sounds like. The buyer typically takes over full ownership of the business. The largest advantage is having an existing blueprint that can include important factors like an established customer base, defined operating expenses, and fully trained employees. Regardless of business type, almost any kind of business could be bought or sold.

When you buy an existing business, you typically get complete control over its direction. However, with no set vision, infrastructure, or external guidance, your business could struggle as you figure out the best way to run things. Again, it is important to seek out supports on advice and guidance.

6. Choose a business structure

Your business structure affects how much you pay in taxes, your ability to raise money, the paperwork you need to file, and your personal liability.

You’ll need to choose a business structure before you register your business with the state. Most businesses will also need to get a VAT number and file for the appropriate licenses.

In Ireland, business structures include:

- Sole Trader.

- Limited Partnership Company (LP)

- Private Company Limited by Shares (LTD)

- Designated Activity Company (DAC)

- Company Limited by Guarantee (CLG)

- Public Limited Company (PLC)

- Choose and register your business name

You’ll want to choose a business name that reflects your brand identity and doesn’t clash with the types of goods and services you offer. In Ireland, you will need to work through the Companies Registration Office and their guidance is as follows:

Registration of a business name is obligatory if any individual or partnership (whether composed of individuals or bodies corporate or any combination of both) or any body corporate carries on business under a name other than their own true names. Its purpose is to make public the identities of those individual(s), partnerships or corporate bodies being the legal entity behind the business name.

Specifically registration of a business name is required if:

- an individual uses a business name which differs in any way from his/her true surname. It makes no difference whether the individuals first name or initials are added. So registration is required if, for example, Mr. John Murphy traded as Murphy Builders but not if he traded as Murphy or John Murphy);

- a firm uses a business name which differs in any way from the true names of all partners who are individuals and the corporate names of all partners which are bodies corporate;

- a company uses a business name which differs in any way from its full corporate name;

- a person having a place of business in the State carries on the business of publishing a newspaper.

Forms to be completed

To register a business name, submit one of the following forms, along with the registration fee (€40 for paper filing/€20 for electronic filing), to the CRO within one month of adopting the business name:

- Form RBN1: for an individual

- Form RBN1A: for a partnership

- Form RBN1B: for a body corporate

7. Registration of a new business for VAT

If you have set up a business but have yet to supply taxable goods or services, you may reclaim VAT on your start-up costs. However, to do so you are required to register for VAT.

This will enable you to obtain credit for VAT on purchases made before trading begins.

Traders whose turnover is below the VAT thresholds and certain businesses (farmers and sea fishers) are not generally obliged to register for VAT. They may, however, elect to register for VAT. Check ‘Further guidance’ at Revenue.ie

8. Open a business bank account

As soon as you start accepting or spending money as your business, you should open a business bank account. Common business accounts include a business current account and business start-up account. Merchant and payment services are also a highly important of a banking service which allow you to accept credit and debit card transactions from your customers.

Some business bank accounts may offer benefits that don’t come with a standard personal bank account but remember to check around to each of the banks to get an exact list of what is on offer to you and your business. Some less discussed benefits of a business bank account are:

- Separation from personal – keeping your business funds separate from your personal funds is important allows you to get a relatively handy snapshot of your business activity.

- Professionalism. Customers will be able to pay you with credit cards and make checks out to your business instead of directly to you. Plus, you’ll be able to authorise employees to handle day-to-day banking tasks on behalf of the business.

- Preparedness. Business banking usually comes with the option for a line of credit for the company. This can be used in the event of an emergency, or if your business needs new equipment.

9. Get business insurance

Business insurance protects you from the unexpected costs of running a business. Accidents, natural disasters, and lawsuits could run you out of business if you’re not protected with the right insurance.

While the protections you get from choosing any of the different forms of business structure will offer varying level of protection to you individually as well as your business from lawsuits, and even that protection is limited.

Business insurance can fill in the gaps to make sure both your personal assets and your business assets are fully protected from unexpected events (natural and manmade).

In some instances, you might be legally required to purchase certain types of business insurance.

Common types of business insurance

- Public Liability Insurance.

- Employers’ Liability Insurance.

- Product Liability Insurance.

- Commercial Property Insurance.

- Business Interruption Insurance.

Make sure you understand which insurance best protects you and your business.

Four steps to buy business insurance

- Assess your risks. Think about what kind of accidents, natural disasters, or lawsuits could damage your business. Assess your risks thoroughly and to make sure you’ve insured every aspect of your business.

- Find a reputable insurance broker. Commercial insurance brokers can help you find policies that match your business needs. They receive commissions from insurance companies when they sell policies, so it’s important to find a licensed agent that’s interested in your needs as much as his/her own.

- Shop around. Prices and benefits can vary significantly. You should compare rates, terms, and benefits for insurance offers from several different agents.

- Re-assess every year. As your business grows, so do your liabilities. If you have purchased or replaced equipment or expanded operations, you should contact your insurance agent to discuss changes in your business and how they affect your coverage.

10. Manage your finances

Accounting for revenue generation and expenses can help keep your business running smoothly. Make sure you maintain proper bookkeeping and have a basic knowledge of business finances. Read more on business finance here.

Start with a balance sheet

The balance sheet is the foundation of managing your finances. It operates as a snapshot of your business financials. It helps you keep track of your capital and provide a cash flow projection for future years.

A balance sheet will help you account for costs like employees and supplies. It will also help you track assets, liabilities, and equity. You can get insights by separating and analyzing segments of your business, like comparing online sales to face-to-face sales.

Cost-benefit analysis (CBA)

Looking closely at money-in and money-out helps maintain a sustainable balance between profit and loss. From development and operations to recurring and nonrecurring costs, it’s important to categorize expenses in your balance sheet. Then, you can use a cost-benefit analysis to weigh the strengths and weaknesses of a business decision, and put potential recurring benefits and cost reductions in context.

A CBA is a technique for making non-critical choices in a relatively quick and easy way. It simply involves adding money in benefits and money in costs over a specified time period, before subtracting costs from benefits to determine success in terms of Euro cost. This can come in handy with hiring another employee or an independent contractor.

For example, let’s say you’re deciding whether to add outdoor seating for your fish themed restaurant, Scales & Waves. You estimate outdoor seating would add €5,000 in extra profit from sales each year. But, the outdoor seating license €1,000 each year, and you’d also have to spend €2,000 to buy outdoor tables and chairs. Your cost-benefit analysis shows that you should add outdoor seating, because the new benefits (€5,000 in new sales) outweigh the new costs (€3,000 in permitting and equipment expenses).

Get accounting help

You might want to get help with your accounting. Consider hiring a qualified and licensed accountant or bookkeeper, or learning how to use an online service.

A chartered accountant will typically cost more than online services, but can normally offer more detailed and personalised service for your specific business needs. A bookkeeper can provide basic day-to-day functions at a lower cost, but won’t possess the formal accounting education of a chartered accountant. You can also access some additional information on which type of accountant might be right for you HERE.

Additional supports – One last point. The ‘Local Enterprise Offices’ are located all over the country and, provide advice and grant assistance to micro enterprises (with employees of 10 or less). To find out more, visit localenterprise.ie

Frank Conway is a Qualified Financial Adviser and has worked with companies in Ireland and the US on credit application and strategy development.

Comments are closed.